Compliance Attributes for the Internal Audit Function - September 2020

Date: September 2020

PDF Version (137 KB, 2 Pages)

Key compliance attributes are published in accordance with the Office of the Comptroller General of Canada (OCG) Technical Bulletin 2018-1: Policy on Internal Audit. It states that:

A.2.2.3 Departments must meet public reporting requirements as prescribed by the Comptroller General of Canada and using Treasury Board of Canada Secretariat prescribed platforms, including:

A.2.2.3.1 Performance results for the internal audit function.

These key compliance attributes demonstrate that the fundamental elements necessary for oversight are in place, are performing as required under the Policy on Internal Audit and the Directive on Internal Audit, and are achieving results.

Key Compliance Attributes

Professional Qualifications

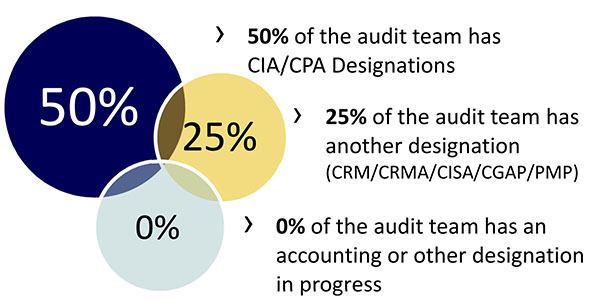

Members of the internal audit team are trained to do their job effectively. Multidisciplinary teams are in place to address diverse risks. The breakdown of the internal audit staff professional qualifications is shown in Figure 1.

Figure 1. Internal audit staff qualifications as of September 30, 2020

Figure 1 – Text version

The bubble chart shows the breakdown of the internal audit staff qualifications as of September 30, 2020.

| Certified Internal Auditor (CIA)/Chartered Professional Accountant (CPA) Designations | 50% |

Other Designations

|

25% |

Accounting or other designation in progress |

0% |

Conformance with the International Standards

The Audit and Assurance Services Branch's internal audit work conforms to international standards for the profession. The last external audit assessment was completed in May 30, 2017. A comprehensive briefing on the most recent internal assessment was presented on March 3, 2020, at the Departmental Audit Committees. The comprehensive briefing consisted of an update on:

- The scope and frequency of both the internal and external assessments

- The qualifications and independence of the assessor(s) or assessment team, including potential conflicts of interest

- Conclusions of assessors

- Corrective action plans

- Internal process, tools and information considered necessary to evaluate conformance with the Institute of Internal Auditor's Code of Ethics and Standards

- Results of the Internal Audit Branch's Quality Assurance and Improvement Program

The internal audits conducted by the Audit and Assurance Services Branch are planned and based on the approved Risk-Based Audit Plans. The audits and the implementation status of their Management Action Plan (MAP) are listed in Table 1. Additions and adjustments to the internal audits may occur in order to address emerging risks and priorities of the organization.

| Internal Audit Title | Status | Report Approved Date |

Report Published Date |

Original planned MAP Completion date |

MAP Implementation status |

|---|---|---|---|---|---|

| Audit of the Implementation of the Staffing Frameworks (previously approved as: Audit of Human Resources Services) | In Progress | - Not Available | - Not Available | - Not Available | - Not Available |

| Audit of Asset Management | In Progress | - Not Available | - Not Available | - Not Available | - Not Available |

| Audit of the Process for Recipient Auditing | In Progress | - Not Available | - Not Available | - Not Available | - Not Available |

| Audit of Exceptional Contracting Limits Authority | In Progress | - Not Available | - Not Available | - Not Available | - Not Available |

Audit of the Special Grant Authority to Provide COVID-19 Funding to the Territories |

In Progress | - Not Available | - Not Available | - Not Available | - Not Available |

| Audit of the CIRNAC COVID-19 Funds Delivered by the Nutrition North Program | In Progress | - Not Available | - Not Available | - Not Available | - Not Available |

Overall Usefulness of Internal Audits

No post-audit survey results were requested or received during this period.